4. Prepare your resume for a civilian job.

To help you find your next job, we've teamed up with Recruit Military Open in New Window. It helps service members and their spouses transitioning out of the military connect with veteran friendly employers looking for top talent.

Updating your resume is an important part of this process. Civilian employers don't necessarily speak or understand military lingo, so if your resume is filled with military jargon or acronyms to your skills, the HR professional on the receiving end likely doesn't have the knowledge to decipher it.

It's important that you describe your skills and military experience in their language so hiring teams can understand how your abilities can benefit their company. Once you've updated your resume, ask a few civilian friends to look at it. If they can understand your strengths and experience, you're probably headed in the right direction.

5. Learn about civilian benefits.

If you feel confused when you hear people discussing high-deductible health care plans or using terms like HSA or FSA, you're not alone.

While it may be confusing, having sufficient health care is important for your financial security. Take some time to understand the differences so you can better compare jobs and benefits packages.

It's important to note that if you're not retiring from the military, you'll need to replace TRICARE.

6. Secure your life insurance.

When you leave the military, your Servicemembers' Group Life Insurance, or SGLI, will go away. However, you’ll still probably need life insurance.

Veterans' Group Life Insurance, or VGLI, is one option for veterans struggling to get life insurance due to health risks, but there may be less expensive alternatives for those who are healthier.

7. Learn about VA disability.

If you have a current illness, disease or injury that was caused or worsened by your military service, file a claim for disability pay. Wartime veterans who meet certain requirements may also qualify for veteran pension benefits. Through the Department of Veterans Affairs, or VA, you can find out if you're eligible and submit a claim Open in New Window.

Suffering from a disability can cost you in ways you may not expect. For example, you may be able to use your disability check to hire help if your injuries or disabilities prevent you from doing them yourself.

It's also hard to predict what types of medical treatments you'll need in the future. Your disability check and VA benefits can help you save on medical expenses down the road.

But the VA disability process can be confusing. The good news is that there are many free services are offered to help veterans navigate the VA disability process, including organizations like:

8. Update your insurance policies.

If you move to a new city, you'll need to update your insurance policies. Some insurance costs are location based, such as auto insurance. Be sure to update your budget to reflect the new insurance premiums.

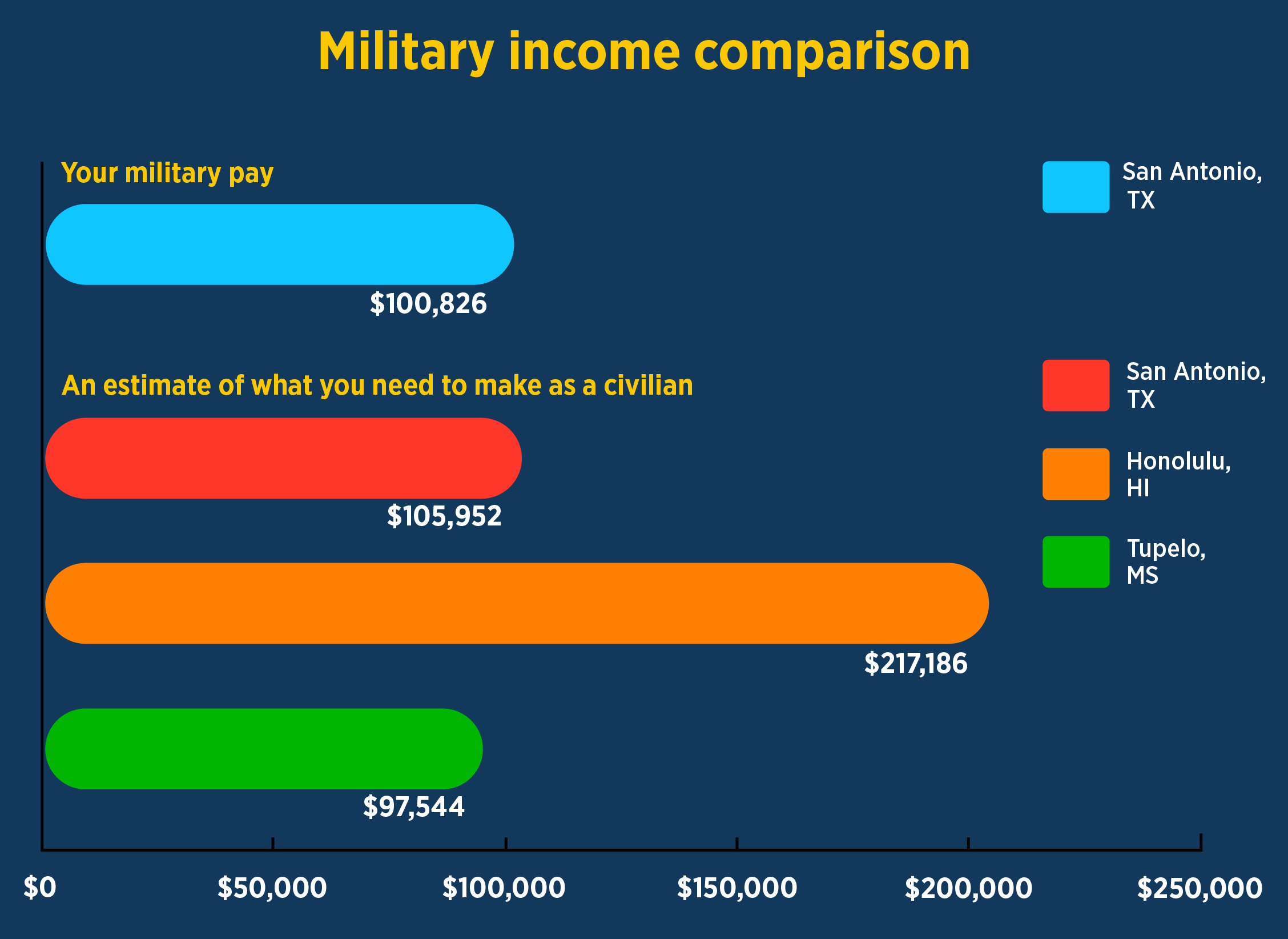

9. Create a civilian budget.

Speaking of budgets, do you have one?

As your separation date nears and you have a clearer picture of life after the military, where you'll live, your new income, and new or changing expenses, create a new civilian budget.

This budget should reflect the realities of your new situation, such as health care costs and state taxes. Many service members establish residency in states that don't have state income taxes, and when they move, the new taxes are a surprise. Be sure to fully understand your take-home pay.

As you update your budget, remember why you're doing it. The goal is to spend less than you earn; otherwise, you're constantly going into debt or reducing savings. That's why it's more important to prepare your finances for the transition to civilian life.

10. Decide on retirement benefits.

When you leave the military, ask yourself the following three questions:

What will I do with my TSP?

Will you leave it where it is or roll it over to another retirement account? Here are five things to consider before moving your TSP.

Will I take the BRS lump sum option?

This question applies if you're separating under the Blended Retirement System. You want to understand the pros and cons.

Should I sign up for the Survivor Benefit Plan?

If someone will be financially disadvantaged in the case of your death, the Survivor Benefit Plan helps ensure that a portion of your military retirement paycheck passes to them. It can be a way to provide financially for those left behind.

If you're retiring from the National Guard or Reserve, your decision is a bit more complicated because of the "gray period," or the time between when you retire and when you turn 60. Make sure you understand your Reserve Component Survivor Benefit Plan choices.

11. Explore options for using your GI Bill.

Depending on your civilian career, you may want to go back to school to learn a few additional skills. Remember that you earned GI Bill benefits. Take some time before you leave the military to learn how you can maximize your education benefits Open in New Window.

12. Stay connected with fellow service members.

Don't underestimate the power of networking; you never know where it may lead.

There's a good chance you've met quite a few people during your military career. Reach out to the ones you've lost touch with and keep in contact with your current associates. They can help you with professional networking, as well as offer personal advice and support on relocating and transitioning.

Consider joining professional networking sites, like LinkedIn, that can help you stay current on news in your industry or desired field.

And in addition to networking, be sure to keep in touch with your military mentors. Maintaining these relationships will help you feel a sense of belonging during your transition.

13. Consider part-time military service.

Even though you’re leaving active duty, you might not be quite ready to totally disconnect from the military. You may be able to balance more time with family and your military career by joining the National Guard or the Reserve.

Not only do you get the joy of continued service, but serving in the Reserves or National Guard also provides the following benefits:

- Access to SGLI, and possibly TRICARE Reserve Select.

- Additional pay for drilling.

- Military retirement, as well as the Reserve Component Survivor Benefit Plan.

Check out these 9 must knows about going into the National Guard or Reserves.

14. Prepare your family.

Returning to civilian life is a challenge not only for military members, but also for military spouses and families. If you're moving, your children may be leaving school friends, and your spouse may be leaving a network of his or her own.

Some departing service members choose to live near their former installations, but that's not always practical. Prioritize keeping up with friends via calls and texts, emails, social media and scheduled meetups. Also, consider maintaining a postmilitary support group to learn about education and job opportunities in the civilian world.

15. Be willing to adapt.

One of the biggest challenges you might face when entering the civilian workforce is a surprising language barrier. You know all about LES, TDY, PME, PCS and DITY, but do you know PTO? That's "paid time off" or "leave" in the military.

Don’t be intimidated by terms you don’t understand in your new workplace. Talk to a peer and ask them to interpret things. Pretty soon, you’ll find yourself speaking their language.

Both at work and at home, focus on the positives as you shift from your military to civilian life. More family time, a regular schedule, no deployments, and the ability to set down roots that won't be pulled up every two to three years are all good things.

Start now, and you'll have plenty of time to prepare for a smooth transition.