Prepare for an earthquake

Take steps to protect yourself, family and friends

The suddenness of an earthquake can catch you off-guard. You should try to know what to do whether you’re at your home, in a building or outside. Practice the steps "Drop, Cover and Hold On Opens in a New Window." See note 1 These steps are recommended in order to reduce or prevent injuries and death during earthquakes.

Make an emergency plan

Create a family emergency communications plan that has an out-of-state contact. Plan where to meet if you get separated.

Prepare emergency supplies. Include a first-aid kit, a radio with extra batteries and a flashlight. Have a fire extinguisher and a whistle in there as well.

Store nonperishable food and a manual can opener, medicines, smartphone chargers, and food and supplies for your pets. Prepare drinking water for your family. Have one gallon of water per person per day. Your supplies should last at least two to three days.

If you’re ordered to evacuate, do so. Follow our evacuation guide for more support.

Prepare your home

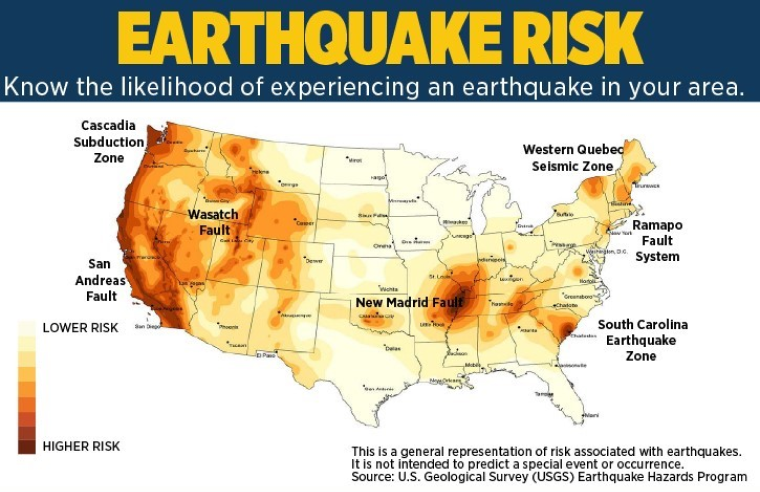

“Great” earthquakes occur only once every five or 10 years. But “strong” or “moderate” earthquakes are more common and can cause a lot of damage.

Earthquakes can be devastating, but you can help reduce the risk of damage to your home and property. Protecting your home starts with reinforcement, bracing, and securing structures and personal property. Take action with the following items in your home:

- Chimneys. A few well-placed metal straps may prevent a masonry chimney from toppling and taking chunks of wall with it, according to the Insurance Institute for Business & Home Safety® Opens in a New Window. See note 1

- Water heaters. Brace your household water heater to the wall. A fallen water heater may expose pipes and lead to flooding. The problem may be even worse if a natural gas line to your water heater ruptures.

- Windows. Install protective safety film — available at most home improvement stores — on the inside of your windows to minimize damage from an earthquake. "If an earthquake breaks your windows, you could have glass shattering everywhere," says Sunde Schirmers, product management director for our Property and Casualty Group.

- House foundations. Consider bracing and bolting your home to the foundation to keep the structure from sliding off the foundation during an earthquake. The California Earthquake Authority™ and Governor's Office of Emergency Services offers a discount program for policies on homes that are braced and bolted to the foundation. A grant is available as well. Learn more about the programs in the following bullets.

Safeguard the interior of your home from earthquakes.

- Secure cabinets, bookshelves and furnishings to walls.

- Install automatic safety shut-off valves to gas and water lines.

- Purchase earthquake-hold museum putty to keep valuable personal items on shelves. Consider moving heavier items to lower shelves.

- Obtain refrigerator locks so the door doesn't shake open, dumping its contents.

Keep in mind that the age and construction of your house also makes a difference. Many newer homes in earthquake hazard areas use updated construction methods to make them earthquake-resistant. And wood-frame houses tend to withstand earthquakes better than brick ones.

Be sure you have the right insurance coverage.

While some homeowners policies cover losses from a fire following an earthquake, homeowners insurance policies generally don't cover losses from earthquakes without additional coverage or a separate policy. Learn more about homeowners insurance and earthquake coverage.

If you think you're at risk, you may consider purchasing a separate policy or an endorsement. An endorsement amends the terms of your original contract and can be issued when you purchase or renew your policy.

Ask yourself the following three questions to determine whether you need coverage if an earthquake strikes.

- Can I afford to repair or rebuild my home?

- Can I afford to replace personal belongings?

- Can I afford temporary housing?

What do earthquake endorsements cover?

Earthquake endorsements may cover repairs needed as a result of earthquake damage, not only to your house but also to other structures on your property, like a garage or shed. Endorsements can also insure the cost to clean up after the earthquake and extra living expenses you incur while you repair the damage.

Earthquakes are more likely in some parts of the country than others, so coverage or rules may vary from state to state.

The California Earthquake Authority provides most earthquake insurance in California. Standardized policies can't be purchased directly through the CEA, but you can purchase them through participating private insurance companies. These policies offer coverage for your dwelling, your personal property and additional living expenses. You can choose between different deductibles and coverage amounts.

Your earthquake deductible is separate from your homeowners deductible — and likely an additional cost. It's important to budget accordingly. You may not be required to pay your deductible before you receive benefits from a claim because your deductible can be subtracted from your total covered losses.

Consider your personal and financial situation when you make your coverage decisions.

Stay safe during an earthquake

Know what to do outside

- Stay outside. Crawl toward open space if you can. Stay away from building exteriors, overhead power lines and trees. Stay there until the shaking stops.

- If you're in a moving vehicle, stop when it's safe to do so. Move your vehicle to the shoulder or curb, away from utility poles, overhead wires, and underpasses or overpasses. Stay in the vehicle, keep your seatbelt on, set the parking brake and turn on your hazard warning lights for visibility.

- Turn on the radio for emergency broadcast information. If a power line falls on the vehicle, stay inside until a trained person removes the wire.

- If you're near the shore, and you feel a strong or long-lasting earthquake, or the water suddenly recedes from the beach, tsunami waves may arrive within minutes. As soon as it's safe to move, immediately go to higher ground or inland away from the coast.

- If you're in a mountainous area or near unstable slopes or cliffs, be aware of falling rocks, debris and landslides.

Know what to do inside

- Don't go outside or try to move more than 5 to 7 feet before getting on the ground.

- Don't stand in a doorway. You're safer under a table. In modern houses, doorways are no stronger than any other part of the house. The doorway doesn't protect you from the most likely source of injury. Most earthquake-related injuries and deaths are caused by falling or flying objects — for example, TVs, lamps, glass or bookcases — or by being knocked to the ground.

- Avoid exterior walls, windows, hanging objects, mirrors, tall furniture, large appliances, and kitchen cabinets with heavy objects or glass. The area near the exterior walls of a building is the most dangerous place. Windows, facades and architectural details are often the first parts of the building to break away.

- If you're seated but can't drop to the floor, bend forward, cover your head with your arms, and hold on to your neck with both hands.

- If you're in bed, stay there. Lie face down to protect vital organs. You’re less likely to be injured by fallen and broken objects by staying where you are.

- In a high-rise building, expect the fire alarms and sprinklers to go off during an earthquake.

Recover from an earthquake

Take steps to protect your personal safety.

Listen to authorities and local news for updates to find out when it's safe to return home and if water is safe to drink.

After an earthquake, the disaster may continue. Expect and prepare for potential aftershocks, landslides or even a tsunami if you live on a coast. Each time you feel an aftershock, drop, cover and hold on.

Know your rights and protect your finances.

Review your insurance contract and any documents that a third party vendor may ask you to sign, such as an assignment of benefits, or AOB. This includes auto windshield repair shops, water extraction or mitigation companies, and other contractors. Signing over your insurance benefits to a contractor or other vendor may seem convenient at the moment, but you may lose control of your claim with that third party.

Inspect your property and assess the damage.

Property damage isn’t always immediately evident. If property damage is found, file a claim. Take photos of any damage before you remove debris or make temporary repairs. Be sure to check for any signs of water leaks, especially in the ceilings. If you need to make temporary repairs to prevent further damage, save the receipts for reimbursement consideration. Avoid making permanent repairs until your claims adjuster has assessed damage.

- The earthquake may have damaged your roof enough to allow water to enter your home. Although not typically covered by insurance, consider hiring a licensed contractor to inspect your roof for damage.

- Protect your property from further damage by covering roof openings, broken windows or doors with tarps or plywood, and save receipts for what you spend for reimbursement consideration.

If your vehicle is damaged by a natural disaster, file a claim.

Take photos of any damage before you remove debris or make temporary repairs. If you need to make temporary repairs to make it safe to drive, save the receipts for reimbursement consideration. If there's only damage to your auto glass, file an auto glass claim. If there's damage to more than just your auto glass, file an auto claim.